Written by Eamonn McElroy, CPA, Atlanta

Published December 19, 2021

Background

IRS Form W-9 is an informational form. It is not filed with the IRS, rather it is used to provide a US taxpayer’s tax identification number to a requester.

If a payor has paid $600 or more in cash, check and/or e-check/EFT to a payee in the ordinary course of their trade or business for services, the payor may have to file an IRS Form 1099-NEC with the IRS to report those payments. As part of their due diligence regarding the potential 1099 filing obligation, the payor should request a completed and signed IRS Form W-9 from the payee. Similarly, if $600 or more in interest has been paid by a payor in the ordinary course of their trade or business, an IRS Form 1099-INT may need to be filed with the IRS to report those payments and an IRS Form W-9 would generally be requested from the payee by the payor. If a taxpayer invests in a business entity (for example, an LLC or corporation), the representatives of the business entity may request an IRS Form W-9 to obtain the taxpayer’s tax identification number and confirm that the taxpayer is not subject to backup withholding.

Filing out the IRS Form W-9 is not as straightforward as it may seem on first glance. This article seeks to provide examples of how an IRS Form W-9 should be filled out based on certain fact patterns. While this article does not detail every entity structure one may find themselves in, it will explore some of the most common entity structures.

Example 1: Limited Liability Company (“LLC”) taxed as a Partnership

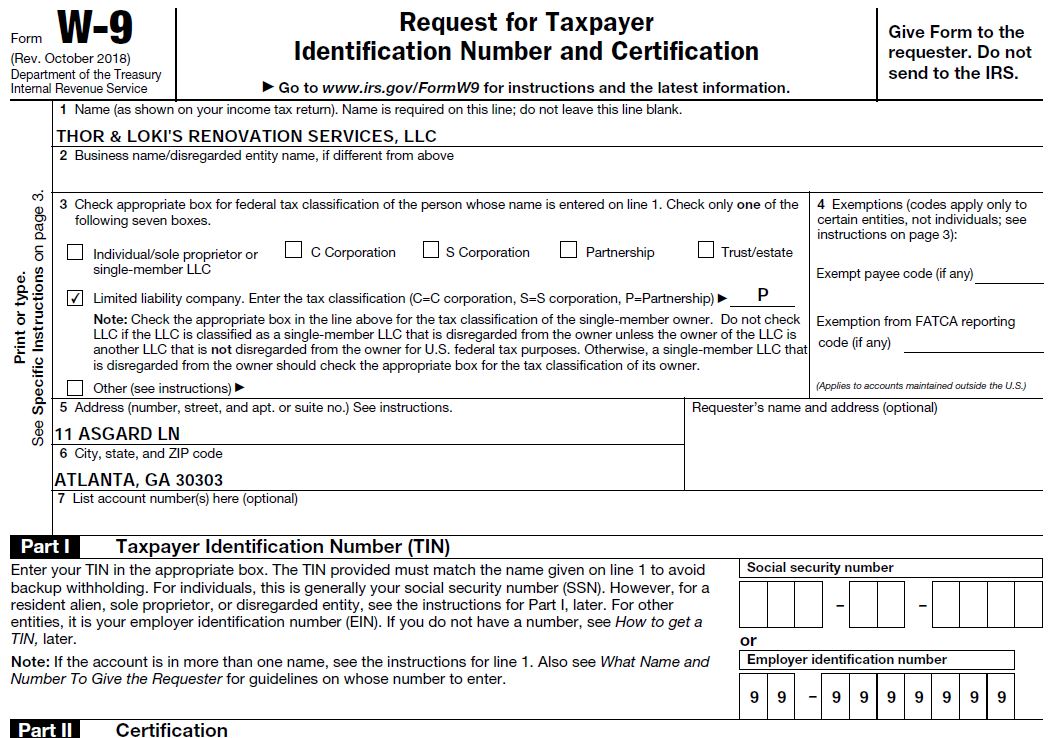

Thor and Loki decide to form an LLC that they will use to provide renovation services. This LLC is organized with the state as “Thor & Loki’s Renovation Services, LLC” and an employer identification number (“EIN”) is subsequently obtained for the LLC.

As both Thor and Loki are members of the LLC, it is a multi-member LLC and, in general, a Partnership by default for federal income tax purposes. The LLC does NOT elect to be treated as a corporation for federal income tax purposes, therefore retaining its default federal income tax classification as a Partnership. The LLC files Form 1065 with the IRS.

If a third-party requested an IRS Form W-9 for Thor & Loki’s Renovation Services, LLC, we would generally expect to see the Form W-9 completed as follows:

- Enter “Thor & Loki’s Renovation Services, LLC” on Line 1

- Leave Line 2 blank

- Check “Limited liability company” and enter “P” on Line 3

- Leave Line 4 blank

- Enter the address of the LLC on Lines 5 & 6

- Leave Line 7 and the Requester’s name and address area blank

- Enter the EIN of the LLC in Part I

Example 2: Limited Partnership (“LP”) taxed as a Partnership

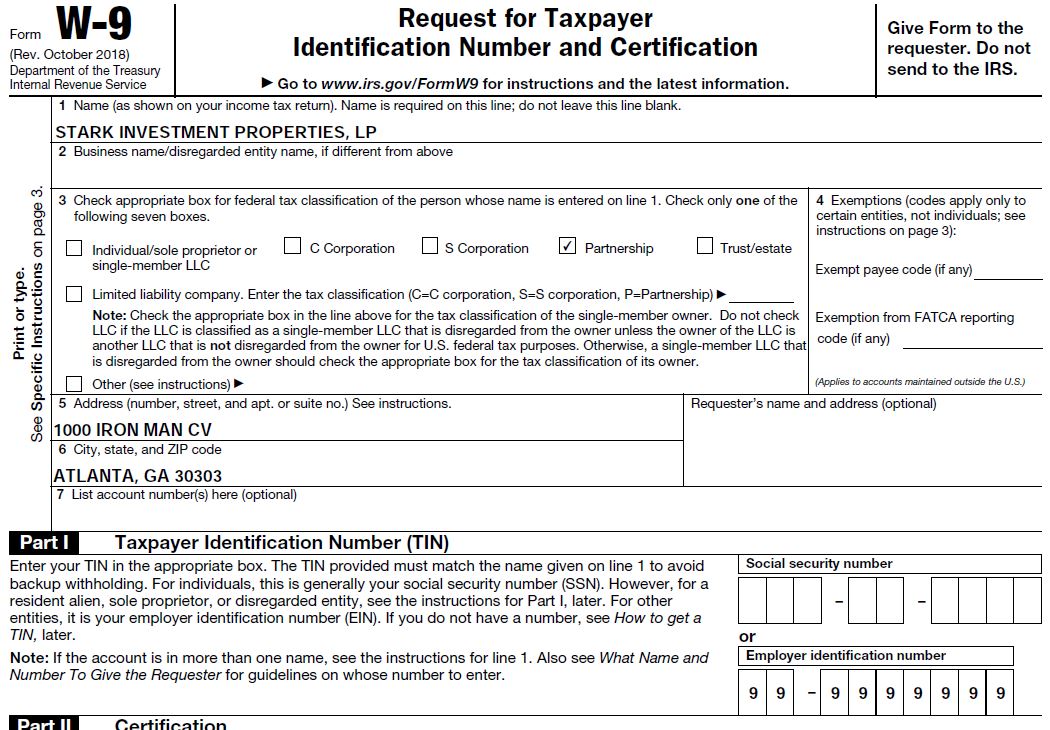

Tony decides to form an LP that he and other investors will use to hold rental real estate. This LP is formed with the state as “Stark Investment Properties, LP” and an employer identification number (“EIN”) is subsequently obtained for the LP.

By default, the LP will be treated as a Partnership for federal income tax purposes. The LP does NOT elect to be treated as a corporation for federal income tax purposes. The LP files Form 1065 with the IRS.

If a third-party requested an IRS Form W-9 for Stark Investment Properties, LP, we would generally expect to see the Form W-9 completed as follows:

- Enter “Stark Investment Properties, LP” on Line 1

- Leave Line 2 blank

- Check “Partnership” on Line 3

- Leave Line 4 blank

- Enter the address of the LP on Lines 5 & 6

- Leave Line 7 and the Requester’s name and address area blank

- Enter the EIN of the LP in Part I

Example 3: Limited Liability Company (“LLC”) taxed as an S Corporation

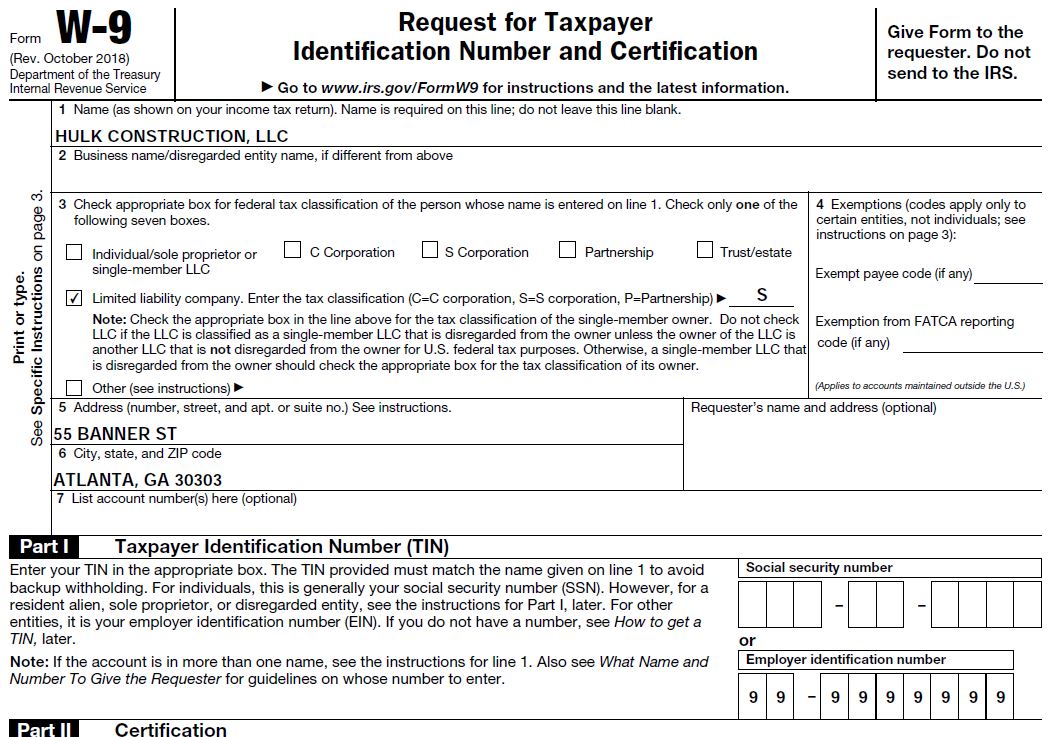

Bruce decides to form an LLC that he will use to provide construction services. This LLC is organized with the state as “Hulk Construction, LLC” and an employer identification number (“EIN”) is subsequently obtained for the LLC.

As Bruce is the sole member of the LLC, it is a single-member LLC and by default treated as a disregarded entity for federal income tax purposes. However, Bruce makes a timely election with the help of his tax advisor to treat the LLC as an S Corporation for federal income tax purposes. The LLC files Form 1120-S with the IRS.

If a third-party requested an IRS Form W-9 for Hulk Construction, LLC, we would generally expect to see the Form W-9 completed as follows:

- Enter “Hulk Construction, LLC” on Line 1

- Leave Line 2 blank

- Check “Limited liability company” and enter “S” on Line 3

- Leave Line 4 blank

- Enter the address of the LLC on Lines 5 & 6

- Leave Line 7 and the Requester’s name and address area blank

- Enter the EIN of the LLC in Part I

Example 4: Corporation taxed as an S Corporation

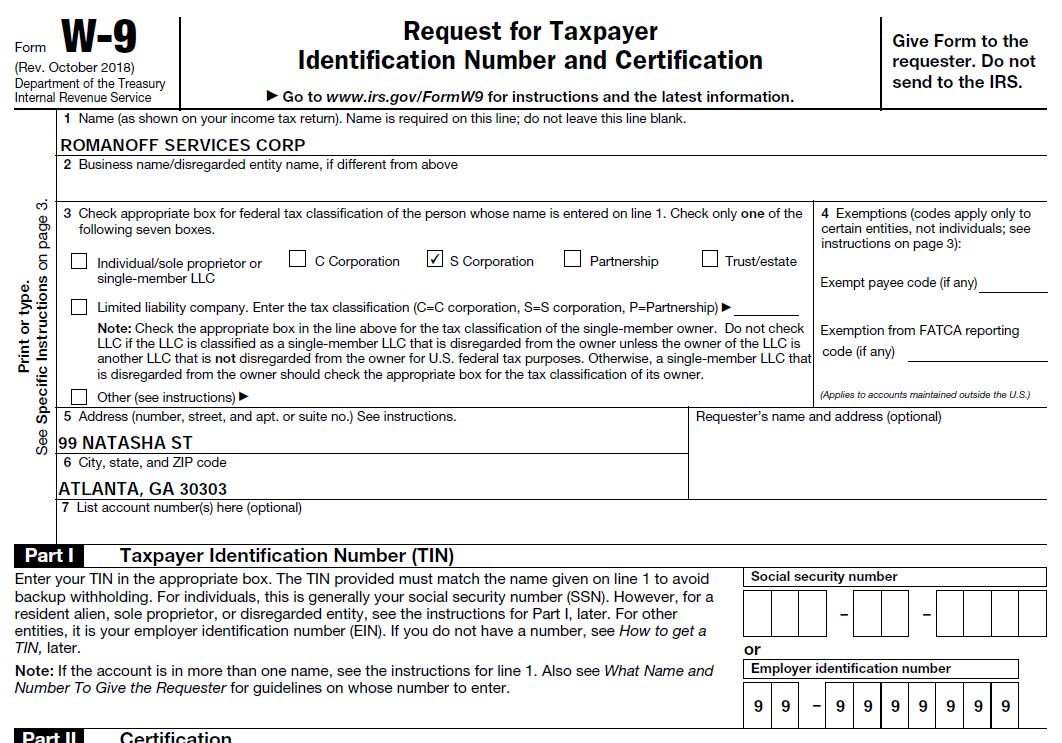

Natasha decides to form a corporation (NOT an LLC) that she will use to provide consulting services. This corporation is incorporated with the state as “Romanoff Services Corp” and an employer identification number (“EIN”) is subsequently obtained for the corporation.

By default, the corporation will be treated as a C Corporation for federal income tax purposes. However, Natasha makes a timely election with the help of her tax advisor to treat the corporation as an S Corporation for federal income tax purposes. The LLC files Form 1120-S with the IRS.

If a third-party requested an IRS Form W-9 for Romanoff Services Corp, we would generally expect to see the Form W-9 completed as follows:

- Enter “Romanoff Services Corp” on Line 1

- Leave Line 2 blank

- Check “S Corporation” on Line 3

- Leave Line 4 blank

- Enter the address of the corporation on Lines 5 & 6

- Leave Line 7 and the Requester’s name and address area blank

- Enter the EIN of the corporation in Part I

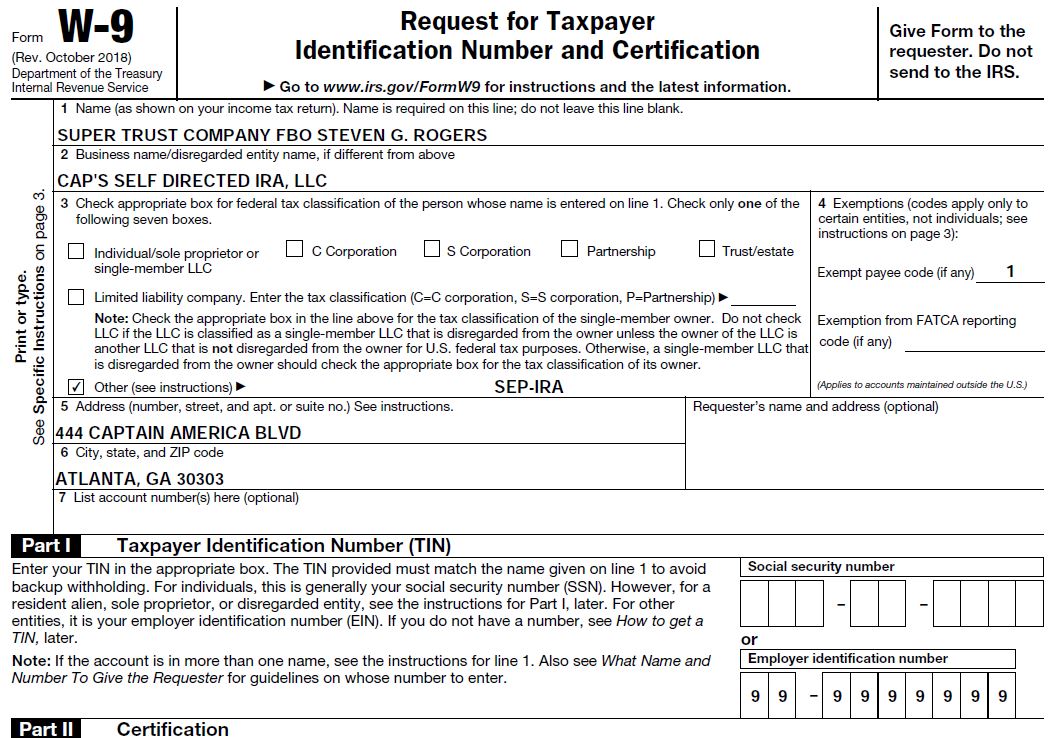

Example 5: Limited Liability Company (“LLC”), owned by a SEP-IRA, taxed as a Disregarded Entity

Steve decides that he would like to use the funds inside his SEP-IRA to invest in alternative assets. To accomplish this, he forms an LLC that will be wholly-owned by his SEP-IRA, and will capitalize this LLC from the SEP-IRA parent. This LLC is organized with the state as “Cap’s Self Directed IRA, LLC” and an employer identification number (“EIN”) is subsequently obtained for the LLC. As Steve’s SEP-IRA is the sole member of the LLC, it is a single-member LLC and by default treated as a disregarded entity for federal income tax purposes (i.e. the LLC will not file a separate income tax return; all activity and assets of the LLC will be reported on the SEP-IRA’s IRS Form 990-T, as applicable).

If a third-party requested an IRS Form W-9 for Cap’s Self Directed IRA, LLC, we would generally expect to see the Form W-9 completed as follows:

- Enter “Super Trust Company FBO Steven G. Rogers” on Line 1 (NOT the LLC, rather the name of the SEP-IRA account as provided by the custodian or plan administrator)

- Enter “Cap’s Self Directed IRA, LLC” on Line 2 (as it is a disregarded entity – the name of the LLC)

- Check “Other” and enter “SEP-IRA” on Line 3

- Enter “1” on the first space and leave the second space blank on Line 4

- Enter the address of the LLC on Lines 5 & 6

- Leave Line 7 and the Requester’s name and address area blank

- Enter the EIN of the SEP-IRA in Part I (NOT the EIN of the LLC, rather the EIN of the entity on line 1 -- the SEP-IRA)

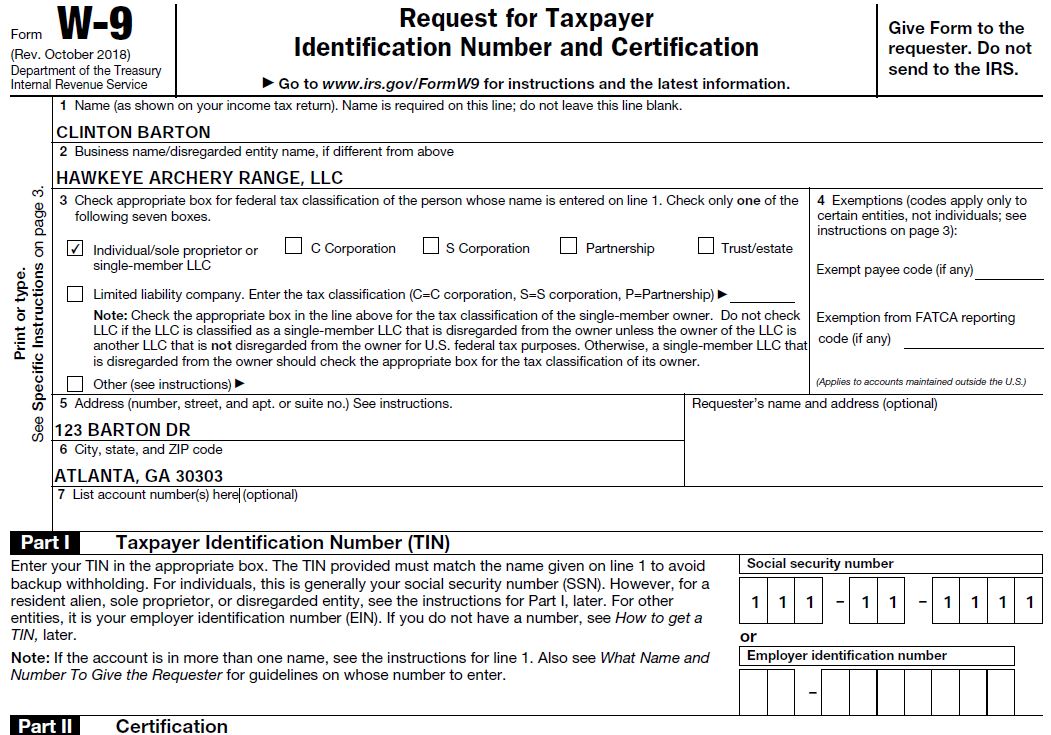

Example 6: Limited Liability Company (“LLC”), owned by an Individual, taxed as a Disregarded Entity

As this situation is quite frequent, perhaps the most frequently encountered W-9 situation at the time this article was originally published, and because more often than not it causes a great deal of confusion and passionate debate surrounding how to fill out a W-9, it’s been saved for last.

The situation referred to is that of an LLC that is wholly-owned by one individual (assume a US citizen or US resident alien for this example), for which an affirmative election to be treated as a corporation for federal income tax purposes has NOT been made. i.e. The LLC is treated as a disregarded entity for federal income tax purposes.

As an aside, please note that the author is not concerned in this article with what may pass through IRS systems. Rather, he is conveying the proper way to fill out an IRS Form W-9 in this situation according to IRS Form W-9 instructions and authoritative guidance existing at the time the article was published. The information conveyed in this example can be corroborated with a careful and thorough reading of the IRS Form W-9 instructions.

Now for our example:

Clint decides to form an LLC that he will use to run a commercial archery range. This LLC is organized with the state as “Hawkeye Archery Range, LLC” and an employer identification number (“EIN”) is subsequently obtained for the LLC.

As Clint is the sole member of the LLC, it is a single-member LLC and by default treated as a disregarded entity for federal income tax purposes (i.e. the LLC will NOT file a separate federal income tax return; all activity and assets of the LLC will be reported on Clint’s IRS Form 1040).

If a third-party requested an IRS Form W-9 for Hawkeye Archery Range, LLC, we would generally expect to see the Form W-9 completed as follows:

- “Clinton Barton” on Line 1 (NOT the LLC’s name, rather the name of the Individual owner as it appears on his or her IRS Form 1040)

- “Hawkeye Archery Range, LLC” on Line 2 (as it is a disregarded entity – the name of the LLC)

- “Individual/sole proprietor or single-member LLC” checked on Line 3

- Line 4 left blank

- Address of the LLC on Lines 5 & 6

- Line 7 and the Requester’s name and address area left blank

- The Social Security Number of the Individual Owner entered in Part I (NOT the EIN of the LLC)

- Yes, you read that correctly, the SSN of the individual owner. If the reader believes this is incorrect, the author kindly asks the reader carefully read the IRS Form W-9 instructions and then use them to work through each line on the IRS Form W-9.

Copyright © 2021 Eamonn McElroy CPA, LLC.

Disclaimer: Tax law, regulation and procedure are constantly changing. Eamonn McElroy CPA, LLC has provided this article as general information only and is under no obligation to update the article for future changes, including but not limited to changes in tax law or procedure. The information contained in the article is not tax, investment or legal advice, nor should it be construed as tax, investment or legal advice. You should consult with your advisors to determine how the information in this article affects you and what actions you may take and should take.